SMM Alumina Morning Comment 6.17

Futures Market: Overnight, the most-traded ag2509 alumina futures contract opened at 2,851 yuan/mt, with a high of 2,870 yuan/mt, a low of 2,839 yuan/mt, and closed at 2,852 yuan/mt, up 7 yuan/mt or 0.24%, with open interest at 306,000 lots.

Ore: As of June 16, the SMM Import Bauxite Index was reported at $74.05/mt, down $0.1/mt from the previous trading day, mainly due to a slight decline in supplier quotes this week compared to earlier periods, leading to a small drop in the SMM Guinea Bauxite CIF Index. However, overall, supplier quotes for bauxite remained at or above $75/mt. The SMM Guinea Bauxite CIF average price was reported at $74.5/mt, unchanged from the previous trading day. The SMM Australia Low-Temperature Bauxite CIF average price was reported at $70/mt, unchanged from the previous trading day. The SMM Australia High-Temperature Bauxite CIF average price was reported at $65/mt, unchanged from the previous trading day.

Industry News:

- According to data on June 13, the total weekly bauxite arrivals at domestic ports were 4.2389 million mt, a decrease of 581,500 mt from the previous week. The total weekly bauxite departures from main ports in Guinea were 4.0746 million mt, an increase of 505,300 mt from the previous week. The total weekly bauxite departures from main ports in Australia were 1.0374 million mt, an increase of 147,700 mt from the previous week.

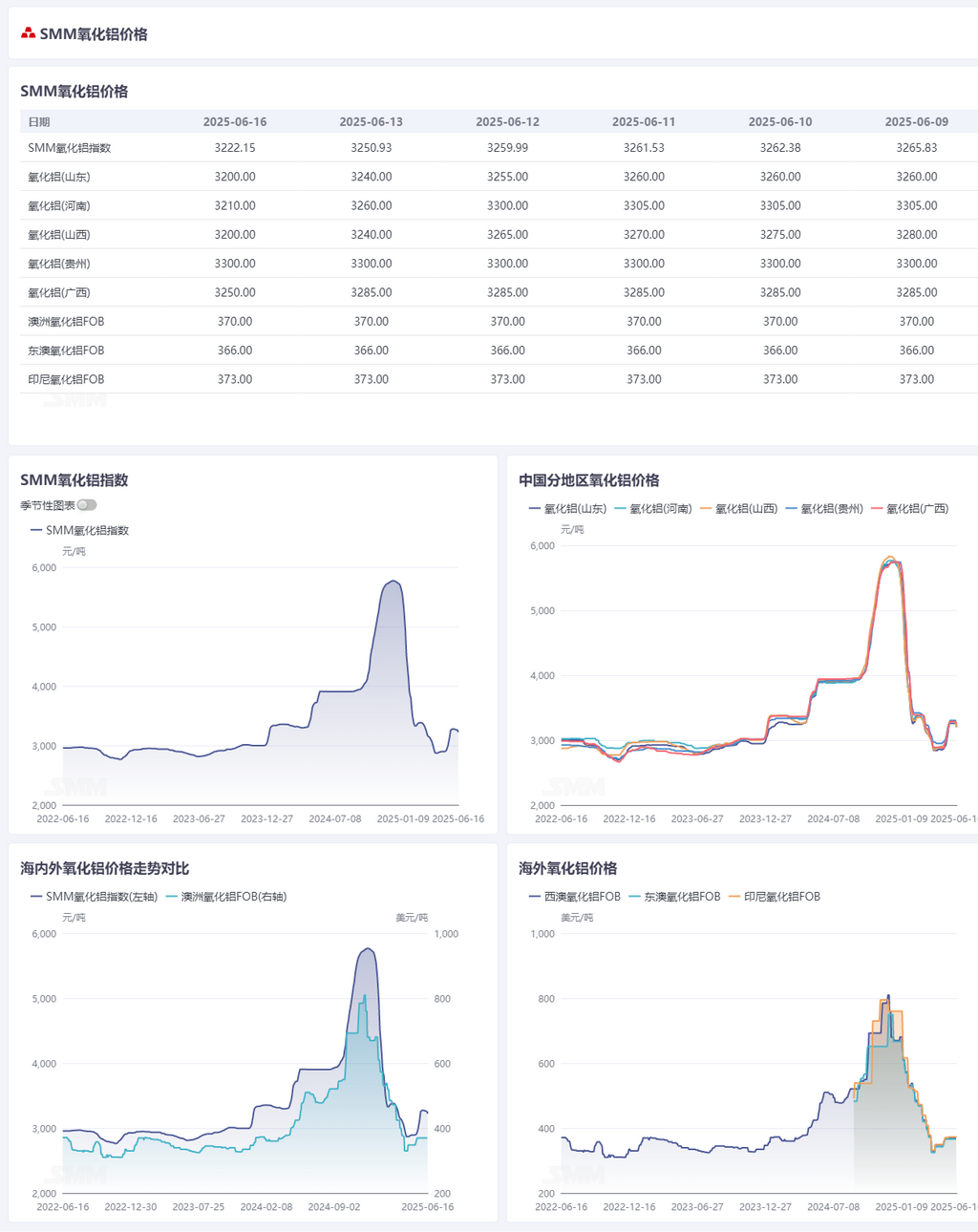

Basis Report: According to SMM data, on June 16, the SMM Alumina Index had a premium of 377.15 yuan/mt against the latest transaction price of the most-traded contract at 11:30.

Warrant Report: On June 16, the total registered alumina warrants remained unchanged from the previous trading day at 80,100 mt. In the Shandong region, the total registered alumina warrants remained unchanged at 601 mt. In the Henan region, the total registered alumina warrants remained unchanged at 300 mt. In the Guangxi region, the total registered alumina warrants remained unchanged at 3,001 mt. In the Gansu region, the total registered alumina warrants remained unchanged at 0 mt. In the Xinjiang region, the total registered alumina warrants remained unchanged at 76,200 mt.

Overseas Market: As of June 16, 2025, the FOB Western Australia alumina price was $370/mt, with an ocean freight rate of $22.00/mt, and the USD/CNY selling rate was around 7.20. This price translates to an external selling price of approximately 3,268 yuan/mt at domestic main ports, which is 46 yuan/mt higher than the domestic alumina price. The alumina import window remained closed.

Summary: Last week, the operating capacity of alumina rebounded by 1.74 million mt/year MoM to 89.01 million mt/year. Spot supply was relatively looser compared to earlier periods, and the total weekly inventory of alumina at aluminum smelters increased by 16,000 mt to 2.646 million mt. In the short term, the alumina fundamentals are expected to maintain a relatively loose pattern. Recently, some ex-factory prices of around 3,100 yuan/mt have been reported in the northern alumina spot market, while sporadic spot transactions have been reported in south-west China, with transaction prices trading at a discount to the online prices. This is expected to drive spot alumina prices to pull back. Going forward, it is necessary to continuously monitor changes in the alumina capacity of domestic enterprises, as well as the supply of imported alumina.

[The information provided is for reference only. This article does not constitute direct advice for investment research and decision-making. Clients should make prudent decisions and should not rely on this information to replace their own independent judgment. Any decisions made by clients are not related to SMM.]